LSTM Single Variate Implementation Approach: Forecasting

Learn more about time series forecasting, a crucial analytical technique that helps businesses and researchers predict future trends based on historical data.

Join the DZone community and get the full member experience.

Join For FreeIn today's data-driven landscape, businesses across industries are continually seeking ways to gain a competitive edge. One of the most powerful tools at their disposal is time series forecasting, a technique that allows organizations to predict future trends based on historical data. From finance to healthcare, time series forecasting is transforming how companies strategize and make decisions.

Time series forecasting involves analyzing data points collected or recorded at specific time intervals. Unlike static data, time series data is chronological, often exhibiting patterns like trends and seasonality. Forecasting methods leverage these patterns to predict future values, providing insights that are invaluable for planning and strategy.

Sales Forecasting

Retail businesses use time series forecasting to predict future sales. By analyzing past sales data, they can anticipate demand, optimize inventory, and plan marketing campaigns.

Stock Market Analysis

Financial analysts employ time series forecasting to predict stock prices and market trends. This helps investors make informed decisions about buying or selling assets.

Weather Prediction

Meteorologists use time series forecasting to predict weather patterns. This data is crucial for agriculture, disaster preparedness, and daily planning.

Healthcare Resource Planning

Hospitals and clinics use forecasting to anticipate patient influx. This helps in managing resources such as staff, beds, and medical supplies.

Energy Consumption Forecasting

Utility companies leverage time series forecasting to predict energy demand. This enables efficient management of power grids and resource allocation.

Forecasting techniques include:

- Statistical Analysis

- Machine Learning Algos like ARIMA

- Neural Networking (RNN): LSTM

LSTM networks are specialized neural networks that handle sequences of data. Unlike regular feedforward neural networks, LSTMs have loops that allow information to persist, making them ideal for tasks where context over time is crucial. Each LSTM cell consists of three parts: an input gate, a forget gate, and an output gate, which regulate the flow of information, allowing the network to selectively retain or forget information over time.

More details can be found in the video "Long Short-Term Memory (LSTM), Clearly Explained."

In this tutorial, we are going to focus on the single variate LSTM analysis. Soon I will be publishing an implementation approach for multivariate analysis.

Main Code

Importing Libraries

import tensorflow as tf

import os

import pandas as pd

import numpy as np

import matplotlib.pyplot as plt

from sklearn.preprocessing import MinMaxScaler

from keras.preprocessing.sequence import TimeseriesGenerator as TSG

from keras.models import Sequential

from keras.layers import Dense

from keras.layers import LSTM

from tensorflow.keras.models import load_model

from tensorflow.keras.callbacks import ModelCheckpoint

import tensorflow.keras.optimizers as optimizers

import seaborn as sns

import statsmodels.api as smLoading the data from the CSV file, this is beverage sales data. Then column update changes Unnamed: 0 to date. Convert the entries in the date column from strings (or any other format they might be in) to datetime objects. The range function generates a sequence of numbers starting from 1 and ending at the total number of entries in the DataFrame (inclusive). This sequence is then assigned to a new column called sequence.

import pandas as pd

# Load data from a CSV file into a DataFrame

dfc = pd.read_csv('sales_beverages.csv')

# Rename the column from 'Unnamed: 0' to 'date'

dfc = dfc.rename(columns={"Unnamed: 0": "date"})

# Convert the 'date' column from a string type to a datetime type to facilitate date manipulation

dfc["date"] = pd.to_datetime(dfc["date"])

# Add a new column called 'sequence' which is a sequence of integers from 1 to the number of rows in the DataFrame

# This sequence helps in identifying the row number or providing a simple ordinal index

dfc["sequence"] = range(1, len(dfc) + 1)

# Display the modified DataFrame

dfc

| DATE | Sales_Beverages | Sequence | |

| 0 | 2016-01-02 | 250510.0 | 1 |

|---|---|---|---|

| 1 | 2016-01-03 | 299177.0 | 2 |

| 2 | 2016-01-04 | 217525.0 | 3 |

| 3 | 2016-01-05 | 187069.0 | 4 |

| 4 | 2016-01-06 | 170360.0 | 5 |

| ... | ... | ... | ... |

| 586 | 2017-08-11 | 189111.0 | 587 |

| 587 | 2017-08-12 | 182318.0 | 588 |

| 588 | 2017-08-13 | 202354.0 | 589 |

| 589 | 2017-08-14 | 174832.0 | 590 |

| 590 | 2017-08-15 | 170773.0 | 591 |

591 rows × 3 columns

Exploring the Data

print('Number of Samples = {}'.format(dfc.shape[0]))

print('Training X Shape = {}'.format(dfc.shape))

print('Index of data set:\n', dfc.columns)

print(dfc.info())

print('\nMissing values of data set:\n', dfc.isnull().sum())

print('\nNull values of data set:\n', dfc.isna().sum())

# Generate a complete range of dates from the min to max

all_dates = pd.date_range(start=dfc['date'].min(), end=dfc['date'].max(), freq='D')

# Find missing dates by checking which dates in 'all_dates' are not in 'df['date']'

missing_dates = all_dates.difference(dfc['date'])

# Display the missing dates

print("Missing dates are ", missing_dates)

Number of Samples = 591 Training X Shape = (591, 3) Index of data set: Index(['date', 'sales_BEVERAGES', 'sequence'], dtype='object') <class 'pandas.core.frame.DataFrame'> RangeIndex: 591 entries, 0 to 590 Data columns (total 3 columns): # Column Non-Null Count Dtype --- ------ -------------- ----- 0 date 591 non-null datetime64[ns] 1 sales_BEVERAGES 591 non-null float64 2 sequence 591 non-null int64 dtypes: datetime64[ns](1), float64(1), int64(1) memory usage: 14.0 KB None Missing values of data set: date 0 sales_BEVERAGES 0 sequence 0 dtype: int64 Null values of data set: date 0 sales_BEVERAGES 0 sequence 0 dtype: int64 Missing dates are DatetimeIndex(['2016-12-25'], dtype='datetime64[ns]', freq=None)

Break the date columns into individual units like, year, month, date, and day of the week to understand if there is any pattern in the sales data.

year: The year part of the datemonth: The month part of the dateday: The day of the monthday_of_week: The name of the day of the week (e.g., Monday, Tuesday)day_of_week_num: The numerical representation of the day of the week (0 for Monday through 6 for Sunday)

# Extract year, month, day, and day of the week

dfc['year'] = dfc['date'].dt.year

dfc['month'] = dfc['date'].dt.month

dfc['day'] = dfc['date'].dt.day

dfc['day_of_week'] = dfc['date'].dt.day_name()

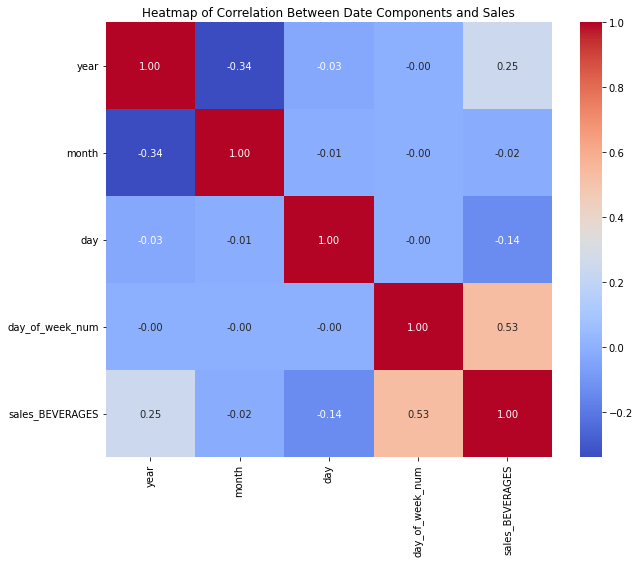

dfc['day_of_week_num'] = dfc['date'].dt.dayofweek A correlation matrix is computed for selected columns (year, month, day, day_of_week_num, and sales_BEVERAGES). This matrix measures the linear relationships between these variables, which can help in understanding how different date components influence beverage sales.

# Calculate correlation matrix

correlation_matrix = dfc[['year', 'month', 'day', 'day_of_week_num', 'sales_BEVERAGES']].corr()

# Print the correlation matrix

#print(correlation_matrix)

# Set up the matplotlib figure

plt.figure(figsize=(10, 8))

# Draw the heatmap

sns.heatmap(correlation_matrix, annot=True, fmt=".2f", cmap='coolwarm', cbar=True)

# Add a title and format it

plt.title('Heatmap of Correlation Between Date Components and Sales')

# Show the plot

plt.show() The code above shows a strong correlation between the sales and days of the week and between the sales and the years. Let's draw the corresponding graphs to verify the variations.

The code above shows a strong correlation between the sales and days of the week and between the sales and the years. Let's draw the corresponding graphs to verify the variations.

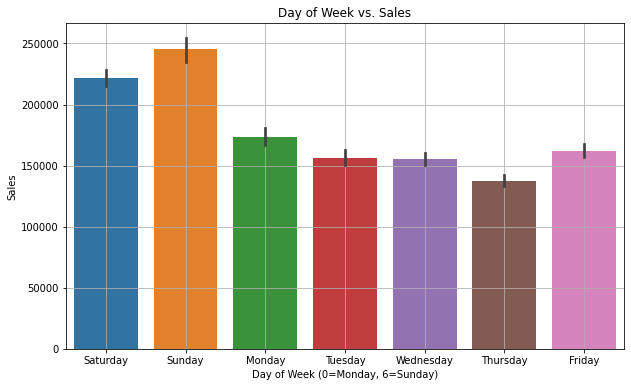

Day of the Week vs. Sales

plt.figure(figsize=(10, 6))

sns.barplot(x='day_of_week', y='sales_BEVERAGES', data=dfc)

plt.title('Day of Week vs. Sales')

plt.xlabel('Day of Week (0=Monday, 6=Sunday)')

plt.ylabel('Sales')

plt.grid(True)

plt.show()

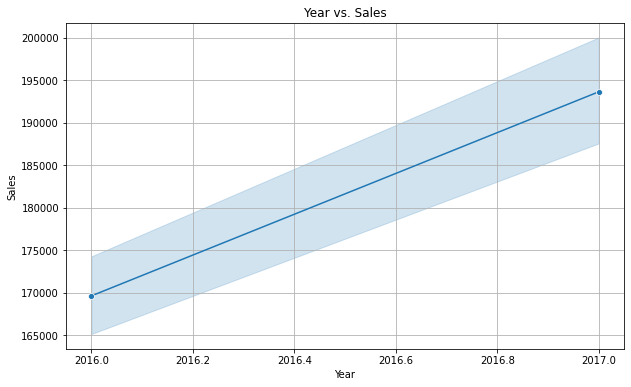

Year vs. Sales

plt.figure(figsize=(10, 6))

sns.lineplot(x='year', y='sales_BEVERAGES', data=dfc, marker='o')

plt.title('Year vs. Sales')

plt.xlabel('Year')

plt.ylabel('Sales')

plt.grid(True)

plt.show()

There is a clear indication that the sales are high on weekends and lesser on Thursdays. Also, yearly sales are increasing every year. It is a linear trend which means there are not many variations.

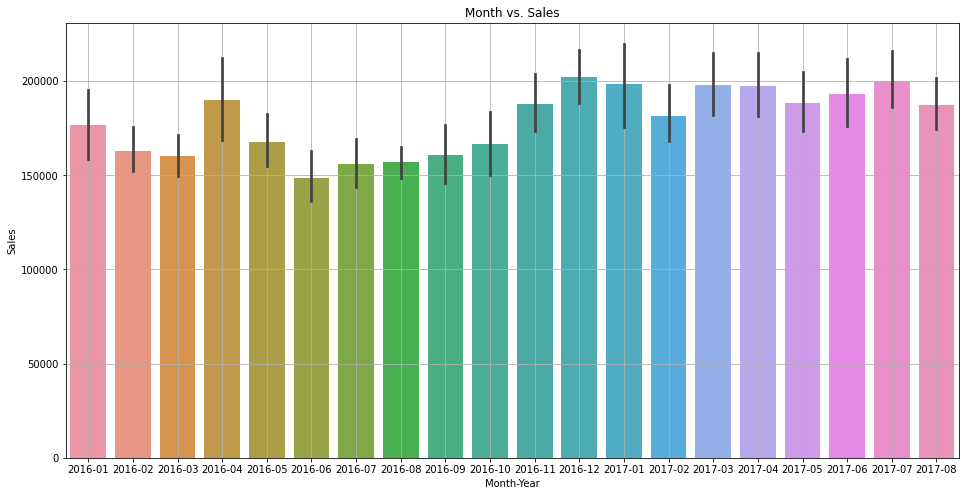

Let's quickly verify the variation with the year-month combination as well.

dfc['month_year'] = dfc['date'].dt.to_period('M')

plt.figure(figsize=(16, 8))

sns.barplot(x='month_year', y='sales_BEVERAGES', data=dfc)

plt.title('Month vs. Sales')

plt.xlabel('Month-Year')

plt.ylabel('Sales')

plt.grid(True)

plt.show()

Due to limited data, it is not very clear, but it seems like sales are higher in the month of December and January.

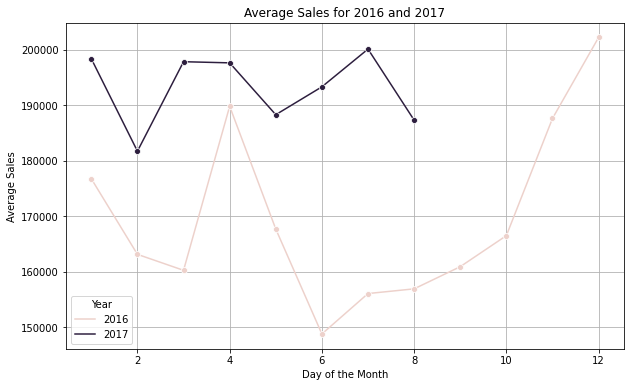

Average Sales Calculation Per Year

#Evaluate the average sales of the year on monthly bais.

a = dfc[dfc['year'].isin([2016,2017])].groupby(["year", "month"]).sales_BEVERAGES.mean().reset_index()

plt.figure(figsize=(10, 6))

sns.lineplot(data=a, x='month', y='sales_BEVERAGES', hue='year', marker='o')

# Enhance the plot with titles and labels

plt.title('Average Sales for 2016 and 2017')

plt.xlabel('Month')

plt.ylabel('Average Sales')

plt.legend(title='Year')

plt.grid(True)

# Show the plot

plt.show()

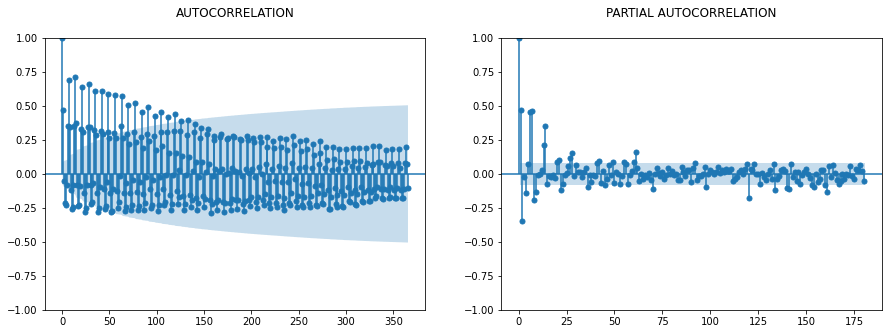

ACF vs PACF (Not Required for LSTM as Such)

This step is generally used with the ARIMA model, but still, it will give you some good visibility around the window size used later.

fig, ax = plt.subplots(1,2,figsize=(15,5))

sm.graphics.tsa.plot_acf(dfc.sales_BEVERAGES, lags=365, ax=ax[0], title = "AUTOCORRELATION\n")

sm.graphics.tsa.plot_pacf(dfc.sales_BEVERAGES, lags=180, ax=ax[1], title = "PARTIAL AUTOCORRELATION\n")

Take out the subset of the data for the trend analysis. Only fetch out the sales_BEVERAGAES, as we are going to perform a single variate analysis in this exercise:

df1=dfc[["date",'sales_BEVERAGES']]

df1.head() date sales_BEVERAGES

0 2016-01-02 250510.0

1 2016-01-03 299177.0

2 2016-01-04 217525.0

3 2016-01-05 187069.0

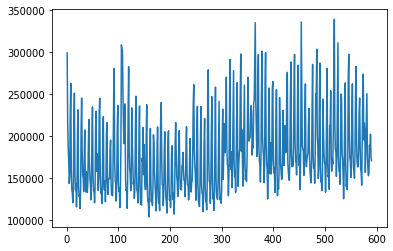

4 2016-01-06 170360.0This line plots the sales_BEVERAGES column from df1, starting from the second element (index 1) to the end. The exclusion of the first data point ([1:]) is used to avoid a specific outlier.

This would filter df1 to only include rows where sales_BEVERAGES is greater than 20,000. Again a step is required to take out the outliers.

plt.plot(df1['sales_BEVERAGES'][1:])

df1=df1[df1['sales_BEVERAGES']>20000]

df2=df1['sales_BEVERAGES'][1:]

df2.shape(589,)

MinMaxScaler

MinMaxScaler is from the sklearn.preprocessing library to scale the data in the df2 series. This is a preprocessing step in data analysis and machine learning tasks, especially when working with neural networks, as it helps to normalize the data within a specified range, typically [0, 1].

X scaled = X max −X min /X−X min

It is used here to improve the convergence process. Many machine learning algorithms that use gradient descent as an optimization technique (e.g., linear regression, logistic regression, neural networks) converge faster when features are scaled. If one feature’s range is orders of magnitude larger than others, it can dominate the objective function and make the model unable to learn effectively from other features.

scaler=MinMaxScaler()

scaler.fit(df2.values.reshape(-1, 1))# Convert the PeriodIndex to DateTimeIndex if necessary

df2=scaler.transform(df2.values.reshape(-1, 1))plt.plot(df2)

I have not used the function below, but still, I have included it with a short explanation. I used the time-series generator instead of it, though both of them will perform the same task. You can use any of them. The function is designed to convert a Pandas DataFrame into input-output pairs (X, y) for use in machine learning models, particularly those involving time series data, such as LSTMs.

window_size: An integer indicating the number of time steps in each input sequence, defaulted to 5df_as_npconverts the Pandas DataFrame to NumPy array to facilitate numerical operations and slicing.- Two lists will be created:

Xfor storing input sequences andyfor storing corresponding labels (output).

It iterates over the NumPy array, starting from the first index up to the length of the array minus the window_size. This ensures that each input sequence and its corresponding output value can be captured without going out of bounds. For each iteration, it extracts a sequence of length window_size from the array and appends it to X. This sequence serves as one input sample. The output value (label) corresponding to each input sequence is the next value immediately following the sequence in the DataFrame. This value is appended to y.

Example:

X=[1,2,3,4,5], y=6

X=[2,3,4,5,6], y=7

X=[3,4,5,6,7], y=8

X=[4,5,6,7,8], y=9

and so on...

def df_to_X_y(df, window_size=5):

df_as_np = df.to_numpy()

X = []

y = []

for i in range(len(df_as_np)-window_size):

row = [[a] for a in df_as_np[i:i+window_size]]

X.append(row)

label = df_as_np[i+window_size]

y.append(label)

return np.array(X), np.array(y)WINDOW_SIZE = 5

X1, y1 = df_to_X_y(df2, WINDOW_SIZE)

X1.shape, y1.shape

print(y1)[143636. 152225. 227854. 263121. 157869. 136315. 132266. 120609. 141955.

220308. 251345. 158492. 136240. 143371. 115821. 135214. 204449. 231483.

141976. 128256. 129324. 113870. 137022. 209541. 245481. 182638. 154284.

149974. 134005. 167256. 207438. 152830. 133559. 157846. 154782. 132974.

144742. 190061. 219933. 166667. 150444. 142628. 124212. 146081. 203285.

234842. 153189. 134845. 137272. 120695. 137555. 208705. 229672. 158195.

179419. 170183. 135577. 152201. 227024. 245308. 155266. 132163. 137198.

119723. 141062. 201038. 223273. 144170. 135828. 147195. 121907. 143712.

202664. 216151. 148126. 130755. 148247. 149854. 149515. 182196. 195375.

143196. 130183. 129972. 129134. 178237. 247315. 280881. 168081. 146023.

145034. 122792. 149302. 209669. 236767. 146607. 134193. 138348. 115020.

136320. 186935. 308788. 303298. 301533. 249845. 213186. 191154. 233084.

238503. 148627. 135431. 136526. 114193. 146007. 232805. 282785. 181088.

161856. 154805. 135208. 155813. 233769. 193033. 167064. 142775. 146886.

125988. 138176. 206787. 247562. 159437. 135697. 133039. 120632. 140732.

198856. 235966. 146066. 118786. 119655. 118074. 173865. 169401. 210425.

154183. 189942. 144778. 136640. 136752. 200698. 237485. 143265. 122148.

123561. 103888. 120510. 177120. 209344. 145511. 122071. 130428. 117386.

138623. 201641. 188682. 156605. 144562. 130519. 110900. 127196. 186097.

211047. 143453. 120127. 120697. 111342. 163624. 221451. 240162. 171926.

141837. 141899. 117203. 137729. 186086. 205290. 148417. 127538. 120720.

108521. 139563. 191821. 206438. 148214. 123942. 128434. 115017. 129281.

178923. 188675. 148783. 124377. 132795. 107270. 133460. 191957. 216431.

180546. 152668. 145874. 128160. 148293. 193330. 206605. 157126. 137263.

138205. 135983. 164500. 166578. 180725. 158646. 147799. 147254. 127986.

150082. 187625. 211220. 155457. 142435. 141334. 124207. 134789. 176165.

197233. 147156. 133625. 145155. 147069. 181079. 238510. 261398. 183848.

164550. 154897. 123746. 138299. 206418. 235684. 145080. 122882. 121120.

116264. 143598. 200090. 235321. 141236. 132262. 129414. 110130. 136138.

192610. 221098. 143488. 122181. 123595. 112182. 142867. 251375. 279121.

172823. 146150. 146410. 120057. 143269. 202566. 247109. 153350. 125318.

129236. 111697. 138234. 197333. 258559. 151406. 129897. 127212. 124603.

144526. 192343. 241561. 142098. 124323. 128716. 120153. 136370. 194747.

232250. 148589. 182070. 215033. 180293. 193535. 208685. 270422. 187162.

166081. 164618. 129184. 150597. 222661. 291398. 165265. 160177. 181322.

138887. 167311. 220970. 278158. 172392. 151843. 157465. 133102. 170648.

223057. 263835. 177635. 140124. 164748. 178953. 185360. 255126. 297968.

182323. 207703. 178510. 140546. 163758. 209125. 260947. 168443. 148518.

159319. 146315. 169151. 226210. 270298. 196844. 194254. 198153. 198308.

226894. 236331. 227027. 177554. 192477. 186177. 240693. 243518. 4008.

335235. 243422. 211239. 175975. 189393. 261820. 297197. 186203. 171274.

164531. 145461. 174206. 252034. 301353. 199820. 184129. 176227. 144535.

162192. 264633. 299512. 191891. 167718. 160219. 125294. 156006. 226837.

257357. 155191. 165171. 192241. 155016. 173306. 256450. 265030. 171537.

156490. 161764. 132978. 164050. 220696. 255490. 169350. 129329. 147599.

137081. 156814. 246049. 213733. 167601. 157364. 148629. 149845. 182391.

230937. 168924. 165020. 212594. 204522. 180400. 186437. 257990. 276118.

169456. 157163. 150271. 147502. 177393. 245596. 288397. 178705. 163684.

173812. 164418. 188890. 259101. 297490. 192579. 172289. 167424. 153886.

182043. 257097. 284616. 188293. 164975. 177997. 136349. 188660. 336063.

264738. 188774. 184424. 181898. 153189. 171158. 228604. 262298. 170621.

163715. 171716. 177420. 179465. 216599. 233163. 175805. 158029. 149701.

144429. 169675. 236707. 285611. 175184. 161949. 164587. 143934. 180469.

250534. 249008. 303807. 200529. 188754. 149629. 161279. 233814. 287104.

166843. 145619. 147196. 135028. 154026. 244193. 206986. 179114. 169098.

165675. 133381. 161718. 227900. 280849. 169143. 151437. 153706. 136779.

212870. 212127. 254132. 171962. 158403. 174304. 166771. 204402. 278488.

339352. 214773. 184706. 181931. 152212. 178063. 242234. 311184. 176821.

158624. 158633. 142765. 181072. 250214. 245520. 179095. 173553. 154251.

125467. 160086. 218486. 263497. 166889. 140339. 143776. 136268. 170346.

271027. 297619. 199766. 173857. 170074. 150965. 178964. 232222. 262375.

179826. 162466. 158262. 149968. 181719. 246513. 283097. 193199. 170182.

163361. 163747. 183117. 229380. 245466. 188077. 160403. 156176. 141686.

191922. 249085. 274030. 195504. 215546. 204566. 156806. 187818. 225481.

250784. 179419. 160636. 153010. 156449. 189111. 182318. 202354. 174832.

170773.]TimeSeriesGenerator

The TimeseriesGenerator utility from the Keras library in TensorFlow is a powerful tool for generating batches of temporal data. This utility is particularly useful when working with sequence prediction problems involving time series data. This aims to simplify the creation of a TimeseriesGenerator instance for a given dataset.

Params

data: The dataset used to generate the input sequencestargets: The dataset containing the targets (or labels) for each input sequence; In many time series forecasting tasks, the targets are the same as the data because you are trying to predict the next value in the same series.length: The number of time steps in each input sequence (specified byn_input).batch_size: The number of sequences to return per batch (set to 1 here, which means the generator yields one input-target pair per batch)

Advantages

Using a TimeseriesGenerator offers several advantages:

- Memory efficiency: It generates data batches on the fly and hence, is more memory-efficient than pre-generating and storing all possible sequences.

- Ease of use: It integrates seamlessly with Keras models, especially when using model training routines like

fit_generator. - Flexibility: It can handle varying lengths of input sequences and can easily adapt to different forecasting horizons.

def ts_generator(dataset,n_input):

generator=TSG(dataset,dataset,length=n_input,batch_size=1)

return generator#Number of steps to use for predicting the next step

WINDOW_SIZE = 30

#This defines the number of features, in our case it is one and it should be sames as the count of neurons in the Dense Layer

n_features=1

generator=ts_generator(df2,WINDOW_SIZE)The code snippet provided iterates over a TimeseriesGenerator object, collecting and aggregating all batches into two large NumPy arrays: X_val for inputs and y_val for targets.

X_val,y_val=generator[0]

for i in range(len(generator)):

X2, Y2 = generator[i]

print("X:", X2)

#print("Y:", type(Y))

X_val = np.vstack((X_val, X2))

y_val = np.vstack((y_val, Y2))

X_val=X_val[1:]

y_val=y_val[1:]

X_val=X_val.reshape(X_val.shape[0],WINDOW_SIZE,n_features)

y_val=y_val.flatten()

print(X_val.shape)

print(y_val)Split this dataset into training, validation, and testing sets based on percentages of the dataset's total length.

#l_percent is set to 85%, marking the cutoff for the training set.

#h_percent is set to 90%, marking the end of the validation set and the beginning of the test set.

l_percent=0.85

h_percent=0.90

#l_cnt is the index at 85% of df2, used to separate the training set from the validation set.

#h_cnt is the index at 90% of df2, used to separate the validation set from the testing set.

l_cnt=round(l_percent * len(df2))

h_cnt=round(h_percent * len(df2))

#Splits for dataset creation

val_sales,val_target=X_val[l_cnt:h_cnt],y_val[l_cnt:h_cnt]

train_sales,train_target=X_val[:l_cnt],y_val[:l_cnt]

test_sales,test_traget=X_val[h_cnt:],y_val[h_cnt:]

print(val_sales.shape,val_target.shape,train_sales.shape,train_target.shape,test_sales.shape,test_traget.shape)

(30, 30, 1) (30,) (502, 30, 1) (502,) (29, 30, 1) (29,)

Setting up a Deep Learning Model Using Keras (TensorFlow Backend) for a Time Series Forecasting Task

The code below sets up a deep learning model using Keras (TensorFlow backend) for a time series forecasting task, integrating callbacks for better training management and defining an LSTM-based neural network.

Callback Setup

EarlyStopping: Stops training when a monitored metric has stopped improving after a specified number of epochs (patience=50); This helps in avoiding overfitting and saves computational resources.ReduceLROnPlateau: Reduces the learning rate when a metric has stopped improving, which can lead to finer tuning of models. It decreases the learning rate by a factor of 0.25 after the performance plateaus for 25 epochs, with the minimum learning rate set to 1e-9 (0.000000001).ModelCheckpoint: It saves the model after every epoch but only if it's the best so far (in terms of the loss on the validation set). It saves only the weights to a directory namedmodel/, which helps in both saving space and potentially avoiding issues when model architecture changes but the training script does not.

Layer Setup

Layer1: The first LSTM layer has 128 units and returns sequences. This means it will return the full sequence to the next layer rather than just the output of the last timestep. This setup is often used when stacking LSTM layers. It uses ReLU activation and includes dropout and recurrent dropout of 0.2 to combat overfitting.Layer2: The second LSTM layer has 64 units and does not return sequences, indicating it's the final LSTM layer and only returns output from the last timestep. Similar to the first LSTM, it uses ReLU activation with dropout and recurrent dropout settings.Layer3: A dense layer with 64 units acts as a fully connected neural network layer following the LSTM layers to interpret the features extracted from the sequences.Layer4: The final dense layer with a single unit is typical for regression tasks in time series, where you predict a single continuous value.

Normally, the ReLU function is used with LSTM layers, but I have seen better results with tanh in the prelim analysis so I included this.

from tensorflow.keras.callbacks import EarlyStopping, ModelCheckpoint, ReduceLROnPlateau

callbacks = [

EarlyStopping(patience=20, verbose=1),

ReduceLROnPlateau(factor=0.25, patience=10, min_lr=0.000000001, verbose=1),

ModelCheckpoint('model/', verbose=1, save_best_only=True, save_weights_only=True)

]

model=Sequential()

model.add(LSTM(128,activation='tanh',dropout=0.2, recurrent_dropout=0.2,return_sequences=True,input_shape=(WINDOW_SIZE,n_features)))

model.add(LSTM(64, activation= 'tanh', dropout=0.2, recurrent_dropout=0.2))

model.add(Dense(64))

model.add(Dense(n_features))

model.summary()Model: "sequential_6"

_________________________________________________________________

Layer (type) Output Shape Param #

=================================================================

lstm_16 (LSTM) (None, 30, 128) 66560

lstm_17 (LSTM) (None, 64) 49408

dense_15 (Dense) (None, 64) 4160

dense_16 (Dense) (None, 1) 65

=================================================================

Total params: 120193 (469.50 KB)

Trainable params: 120193 (469.50 KB)

Non-trainable params: 0 (0.00 Byte)

_________________________________________________________________

Compile a Keras model with specific settings for the optimizer, loss function, and evaluation metrics.

Optimizer

optimizers.Adam(lr=.000001): This specifies the Adam optimizer with a learning rate (lr) of 0.000001. Adam is an adaptive learning rate optimization algorithm that has become the default optimizer for many types of neural networks because it combines the best properties of the AdaGrad and RMSProp algorithms to handle sparse gradients on noisy problems.- Learning rate: Setting the learning rate to a very small value, like 0.000001, makes the model training take smaller steps to update weights, which can lead to very slow convergence. This low value is used when you need to fine-tune a model or when training a model where larger steps might cause the training process to overshoot the minima.

Loss Function

loss='mse': This sets the loss function to Mean Squared Error (MSE), which is commonly used for regression tasks. MSE computes the average squared difference between the estimated values and the actual value, making it sensitive to outliers as it squares the errors.

# Compile the model

#cp1 = ModelCheckpoint('model/', save_best_only=True)

model.compile(optimizer=optimizers.Adam(lr=.000001), loss= 'mse', metrics = ['mean_squared_error'])It specifies how the training should be conducted, including the datasets to be used, the number of training epochs, and any callbacks that should be applied during the training process.

epochs=200: The number of times the model will work through the entire training dataset

model.fit(train_sales, train_target, validation_data=(val_sales, val_target) ,epochs=200, callbacks=callbacks)Epoch 1/200 16/16 [==============================] - 1s 72ms/step - loss: 0.0055 - mean_squared_error: 0.0055 - val_loss: 0.0110 - val_mean_squared_error: 0.0110 Epoch 2/200 16/16 [==============================] - 2s 98ms/step - loss: 0.0063 - mean_squared_error: 0.0063 - val_loss: 0.0067 - val_mean_squared_error: 0.0067 Epoch 3/200 16/16 [==============================] - 1s 71ms/step - loss: 0.0062 - mean_squared_error: 0.0062 - val_loss: 0.0119 - val_mean_squared_error: 0.0119 Epoch 4/200 16/16 [==============================] - 1s 71ms/step - loss: 0.0058 - mean_squared_error: 0.0058 - val_loss: 0.0097 - val_mean_squared_error: 0.0097

training_loss_per_epoch: This retrieves the training loss for each epoch from the model's history object. The training loss is a measure of how well the model fits the training data, decreasing over time as the model learns.validation_loss_per_epoch: Similarly, this retrieves the validation loss for each epoch. Validation loss measures how well the model performs on a new, unseen dataset (validation dataset), which helps to monitor for overfitting.- Overfitting: If your training loss continues to decrease, but your validation loss begins to increase, this may indicate that the model is overfitting to the training data.

- Underfitting: If both training and validation losses remain high, this might suggest that the model is underfitting and not learning adequately from the training data.

- Early stopping: By examining these curves, you can also make decisions about using early stopping to halt training at the optimal point before the model overfits.

training_loss_per_epoch=model.history.history['loss']

validation_loss_per_epoch=model.history.history['val_loss']

plt.plot(range(len(training_loss_per_epoch)),training_loss_per_epoch)

plt.plot(range(len(validation_loss_per_epoch)),validation_loss_per_epoch)load_model is a function from Keras that allows you to load a complete model saved in TensorFlow's Keras format. This includes not only the model's architecture but also its learned weights and its training configuration (loss, optimizer).

from tensorflow.keras.models import load_model

model1=load_model('model/')Fetching out the dates from the original DataFrame to set it in the predictions for visibility. Since we are using the window size of 30, the first output/target/prediction will be generated after window_size. Accordingly, manipulate the dates for all three datasets.

The below code is designed to extract specific date ranges from a DataFrame to align them with corresponding training, validation, and test datasets. This is particularly useful when you want to track or analyze results over time or relate them to specific events or changes reflected by dates.

date_df=df1[df1['sales_BEVERAGES']>20000]

date_df.count()

####Fetching the dates from the df1 for the train dataset

train_date=date_df['date'][WINDOW_SIZE - 1:l_cnt + WINDOW_SIZE - 1]

print(train_date.count())

####Fetching the dates from the df1 for the val dataset

val_date=date_df['date'][l_cnt + WINDOW_SIZE - 1:h_cnt + WINDOW_SIZE - 1:]

print(val_date.count())

u_date=h_cnt + 1 + WINDOW_SIZE -1

test_date=df1['date'][h_cnt + WINDOW_SIZE - 1: ]

test_date.count()502 30

29

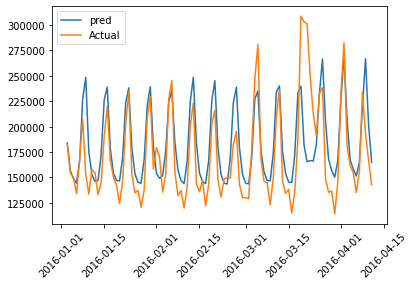

Training Data Actual Value vs Predicted Value

#This function is used to generate predictions from your pre-trained model on the train_sales dataset.

train_predictions = model1.predict(train_sales).flatten()

# Applies the inverse transformation to the scaled predictions to bring them back to their original scale.

train_pred=scaler.inverse_transform(train_predictions.reshape(-1, 1))

t=scaler.inverse_transform(train_target.reshape(-1, 1))

#print(train_pred.shape)

#Creating a dataframe with Actual and predictions

train_results = pd.DataFrame(data={'Train Predictions':train_pred.flatten(), 'Actuals':t.flatten(),'dt':train_date })

train_results.tail(20)16/16 [==============================] - 0s 14ms/step (502, 1)

| Train Predictions | Actuals | dt | |

|---|---|---|---|

| 512 | 195323.593750 | 171962.000000 | 2017-05-29 |

| 513 | 164753.343750 | 158403.000000 | 2017-05-30 |

| 514 | 155985.328125 | 174304.000000 | 2017-05-31 |

| 515 | 153953.828125 | 166771.000000 | 2017-06-01 |

| 516 | 184015.109375 | 204402.000000 | 2017-06-02 |

| 517 | 246616.375000 | 278488.000000 | 2017-06-03 |

| 518 | 251735.953125 | 339352.000000 | 2017-06-04 |

| 519 | 187089.109375 | 214773.000000 | 2017-06-05 |

| 520 | 169009.390625 | 184706.000000 | 2017-06-06 |

| 521 | 160138.390625 | 181931.000000 | 2017-06-07 |

| 522 | 158093.562500 | 152212.000000 | 2017-06-08 |

| 523 | 186708.203125 | 178063.015625 | 2017-06-09 |

| 524 | 254521.234375 | 242234.000000 | 2017-06-10 |

| 525 | 263513.468750 | 311184.000000 | 2017-06-11 |

| 526 | 191338.093750 | 176820.984375 | 2017-06-12 |

| 527 | 168676.562500 | 158624.000000 | 2017-06-13 |

| 528 | 158633.203125 | 158633.000000 | 2017-06-14 |

| 529 | 153251.765625 | 142765.000000 | 2017-06-15 |

| 530 | 180730.171875 | 181071.984375 | 2017-06-16 |

| 531 | 251409.359375 | 250214.000000 | 2017-06-17 |

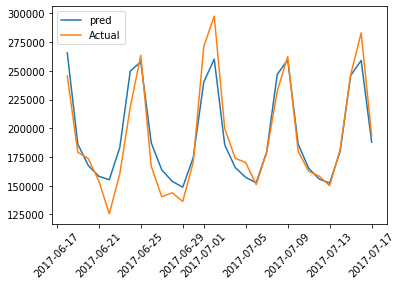

Below is a graphical representation of actual and predicted values of the training data for the first 100 pointers:

plt.plot(train_results['dt'][:100],train_results['Train Predictions'][:100],label='pred')

plt.plot(train_results['dt'][:100],train_results['Actuals'][:100],label='Actual')

plt.legend()

plt.xticks(rotation=45)

plt.plot(figsize=(18,10))

plt.show()

Validation Data Actual Value vs Predicted Value

##This function is used to generate predictions from your pre-trained model on the validation dataset.

val_predictions = model1.predict(val_sales).flatten()

# Applies the inverse transformation to the scaled predictions to bring them back to their original scale.

val_pred=scaler.inverse_transform(val_predictions.reshape(-1, 1))

v=scaler.inverse_transform(val_target.reshape(-1, 1))

print(val_pred.shape)

#Creating a dataframe with Actual and predictions

val_results = pd.DataFrame(data={'Val Predictions':val_pred.flatten(), 'Actuals':v.flatten(),'dt':val_date })

val_results.head()1/1 [==============================] - 0s 62ms/step (30, 1)

| Val Predictions | Actuals | dt | |

|---|---|---|---|

| 532 | 265612.906250 | 245519.984375 | 2017-06-18 |

| 533 | 186157.468750 | 179094.984375 | 2017-06-19 |

| 534 | 167559.578125 | 173553.000000 | 2017-06-20 |

| 535 | 158167.000000 | 154251.000000 | 2017-06-21 |

| 536 | 155162.000000 | 125467.000000 | 2017-06-22 |

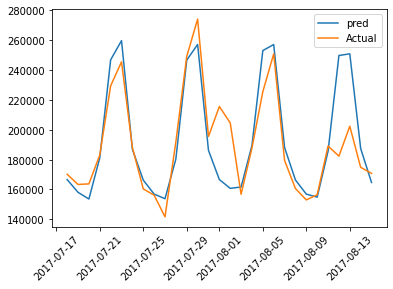

Below is a graphical representation of actual and predicted values of the validation data:

plt.plot(val_results['dt'],val_results['Val Predictions'],label='pred')

plt.plot(val_results['dt'],val_results['Actuals'],label='Actual')

plt.legend()

plt.xticks(rotation=45)

plt.plot(figsize=(18,10))

plt.show()

Test Data Actual Value vs Predicted Value

#This function is used to generate predictions from your pre-trained model on the test dataset.

test_predictions = model1.predict(test_sales).flatten()

# Applies the inverse transformation to the scaled predictions to bring them back to their original scale.

test_pred=scaler.inverse_transform(test_predictions.reshape(-1, 1))

te=scaler.inverse_transform(test_traget.reshape(-1, 1))

print(test_pred.shape)

#Creating a dataframe with Actual and predictions

test_results = pd.DataFrame(data={'Test Predictions':test_pred.flatten(), 'Actuals':te.flatten(),'dt':test_date })

test_results.head()1/1 [==============================] - 0s 35ms/step (29, 1)

| Test Predictions | Actuals | dt | |

|---|---|---|---|

| 562 | 166612.140625 | 170182.000000 | 2017-07-18 |

| 563 | 158095.812500 | 163361.000000 | 2017-07-19 |

| 564 | 153619.515625 | 163747.000000 | 2017-07-20 |

| 565 | 181217.421875 | 183117.015625 | 2017-07-21 |

| 566 | 246784.828125 | 229380.000000 | 2017-07-22 |

plt.plot(test_results['dt'],test_results['Test Predictions'],label='pred')

plt.plot(test_results['dt'],test_results['Actuals'],label='Actual')

plt.legend()

plt.xticks(rotation=45)

plt.plot(figsize=(18,10))

plt.show()

Opinions expressed by DZone contributors are their own.

Comments